Venture Capital Market Update

Market Backdrop

To date, the economy has proven to be more resilient than many had anticipated and there is still a small chance that we might achieve a soft landing, despite rates remaining higher for longer than expected. However, despite the relative health of the economy for now, the funding market for startups has been and continues to be extremely challenging. Capital deployment has dried up across the board and sales cycles have extended with companies being hesitant to invest in growth given the market turmoil over the past 12-18 months and the uncertainty that lies ahead.

We believe that there is much less dry powder available than many are assuming and even less is going to materialize through new and returning funds. If this is the case, it will likely further exacerbate the situation, as LP liquidity continues to be challenged with limited distributions and persistent capital calls.

VC Fundraising

According to Pitchbook, $33.2b was raised for Venture Capital (“VC”) funds through H1 2023 across 233 funds, a six-year low; emerging managers raised only $6.4b in commitments. In general, emerging managers have not been operating for long enough to have had significant track records or distributions, and it is likely that they invested at or near peak valuations. This will make it difficult to raise subsequent funds and we expect to see many of these managers postpone raising capital from investors until markets improve. For the funds that are raising capital, the process is taking longer and often results in smaller raises than expected. In addition, many funds have slowed their deployment cycles to extend their own runways.

The slowing of new fund formation combined with smaller fund raises and slower deployment is a real cause for concern about how portfolio companies will be able to raise at almost every stage over the next 12- to 18-months. Since a considerable number of funds have exhausted their capacity and/or willingness to bridge their investments, any startups hoping to raise will likely be forced to take in new capital from outside investors. Whether they will be open to down-rounds and re-organizations will dictate their survival.

The AI Effect

The first half of the year was buoyed by the hype around Generative AI related startups, which inflated stats pertaining to startup fundraising. For a few months irrational exuberance saw investors invest in anything GenAI related, oftentimes pre-product and pre-revenue. After a few months, most investors have wised up to the fact that many companies were simply stitching together publicly available technology from OpenAi (or other AI providers) with a simple interface. These are simply wrappers with no defensibility.

The AI hype is reflected in data from Carta (The VC industry’s deal database) that shows that the amount of venture dollars raised increased by 26% in Q2, however the total number of deals stayed relatively flat. This means that the average investment size also increased, growing from about $10.4 million in Q1 to $13.1 million in Q2. Despite the lift in numbers driven by the AI boom, at the halfway point, 2023 is on pace to be the quietest year for venture activity since at least 2018. What is not always apparent in the data though are any convertible notes that converted into those growing rounds. Thus, that data must be viewed with some suspicion as it is likely that rounds were smaller and only achieved growth milestones due to convertible notes going into the final numbers. Note also that reported capital raised is usually a trailing number and thus some of that capital was raised and spent a while ago.

Deal Data

Carta data clearly shows that after seeing declines from the peak in 2022, Seed and Series A stage valuations ticked up in Q2 this year, but the absolute deal count declined significantly. This was driven by a combination of GenAI hype and larger funds, which are less valuation sensitive, investing at earlier stages.

However, nearly 19% of all primary fundings on Carta in Q2 were reported down-rounds, confirming that valuation expectations are starting to reset lower. It is worth nothing that what is not readily reported are the shadow down-rounds that happen due to liquidation preferences and pay to play rounds.

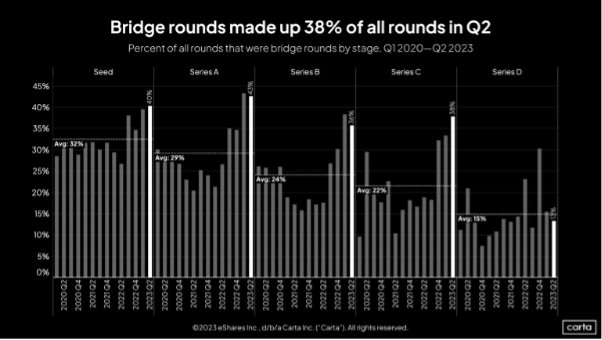

Later stage deal activity continues to be anemic. This is due, in part, to the sheer amount of capital that portfolio companies raised over the past three years. As the focus has shifted from “growth at all costs” to “path to profits”, many portfolio companies have cut expenses, implementing multiple rounds of Reductions in Force (“RIFs”) and, where possible, raising capital from existing investors. These Bridge Rounds allow portfolio companies to wait out the next 18- to 24-months as they try to grow into the valuation set from their last round. Given these dynamics, it is likely that the majority of pain for later stage companies will not be felt until well into 2024.

Conclusion

Despite a stronger than expected economy, our viewpoint is that the next couple of quarters will be very tough for portfolio companies trying to raise capital. As previously explained, we think the capacity for VC’s to lead and price deals will be much diminished and the appetite and ability of insiders to continue to fund their companies is beginning to run out.

Following the market turmoil earlier this year, driven in part by the collapse of Silicon Valley Bank, VC fund’s focus has shifted to investing in companies building real businesses with a clear and near-term path to profitability. After many years of growth at all costs, many companies will not be able to make that shift and their viability as a going concern will be a real challenge.

Many companies that never really had a sustainable business or founders who are not receptive to the new realities will likely go out of business. That may bring a silver lining as it 1) frees up talent and resources 2) ensures that only the best companies look to raise capital and 3) should offer more attractive entry points as valuation expectations continue to be reset lower.

Despite the current market challenges, as in all markets, fundamentally good companies at fair prices will continue to be attractive investments. Given early stage investing continues to have a high degree of risk, we believe that, in this environment, funds deploying venture capital must ensure they focus on investing in real businesses while maintaining price discipline and a cautious underwriting approach.