Deal Sourcing and Underwriting: Understanding a Key Part of the Ballast Rock “Special Sauce”

A Comprehensive Look at Underwriting Process

At Ballast Rock we pride ourselves in our process-oriented approach to sourcing, underwriting, and acquiring real estate. The “secret sauce” to our success comes from our deep relationships with sellers and brokers in the Southeast, our attention to detail, and our boots on the ground approach to acquisition and management. In this educational article, we briefly discuss each of the steps involved from the moment we hear about opportunities to getting to the closing table and putting the property under management.

Stages

Deal Sourcing:

Whether it is through our monthly check-in to inquire about off-market opportunities, fully marketed e-mail blasts, or getting the early look on fully marketed deals, we review countless opportunities every week. That said, only about 1/3 of the opportunities we see pass our initial “deal sourcing” phase:

Price – we are currently only interested in deals that are >$5m or <$20m

Vintage – we primarily only have interest in deals built between the years 1965 and 2000

Capital concentration - we don’t invest in primary markets in the Southeast because there is simply too much capital chasing deals in those location.

Job Concentration – we stay away from markets that have a high concentration of hospitality and food and beverage jobs

“Feds, Meds, and Eds” Employment - we look for cities with federal or state government employment, the healthcare sector is typically the primary employer, and there are one or multiple universities or colleges as significant employers

High-Level Deal Analysis:

After we’ve determined the deal fits our size, vintage, and geography, we discuss specifics with the origination team. The main items we focus on at this stage are as follows:

Price per unit – we stay away from deals that are trading above or close to approximately 2/3 the current cost of new construction as it leaves no room for upside.

Cap rate – at this stage of the market cycle, we are targeting 4.5 – 5.5%+ Caps. the graph above shows the overall decrease in treasury rates and the corresponding decrease in Cap rate spread since the early 2000s.

Location within cities – Ideally, we look for an Average Median Income (AMI) in the $40-50k+ range as well as a heavy concentration of medical and educational jobs.

Above is the demographic data from our Spring Lake property (recently acquired in SB2) in Leesburg, GA that we pull from Costar.

First-Pass Deal Underwriting:

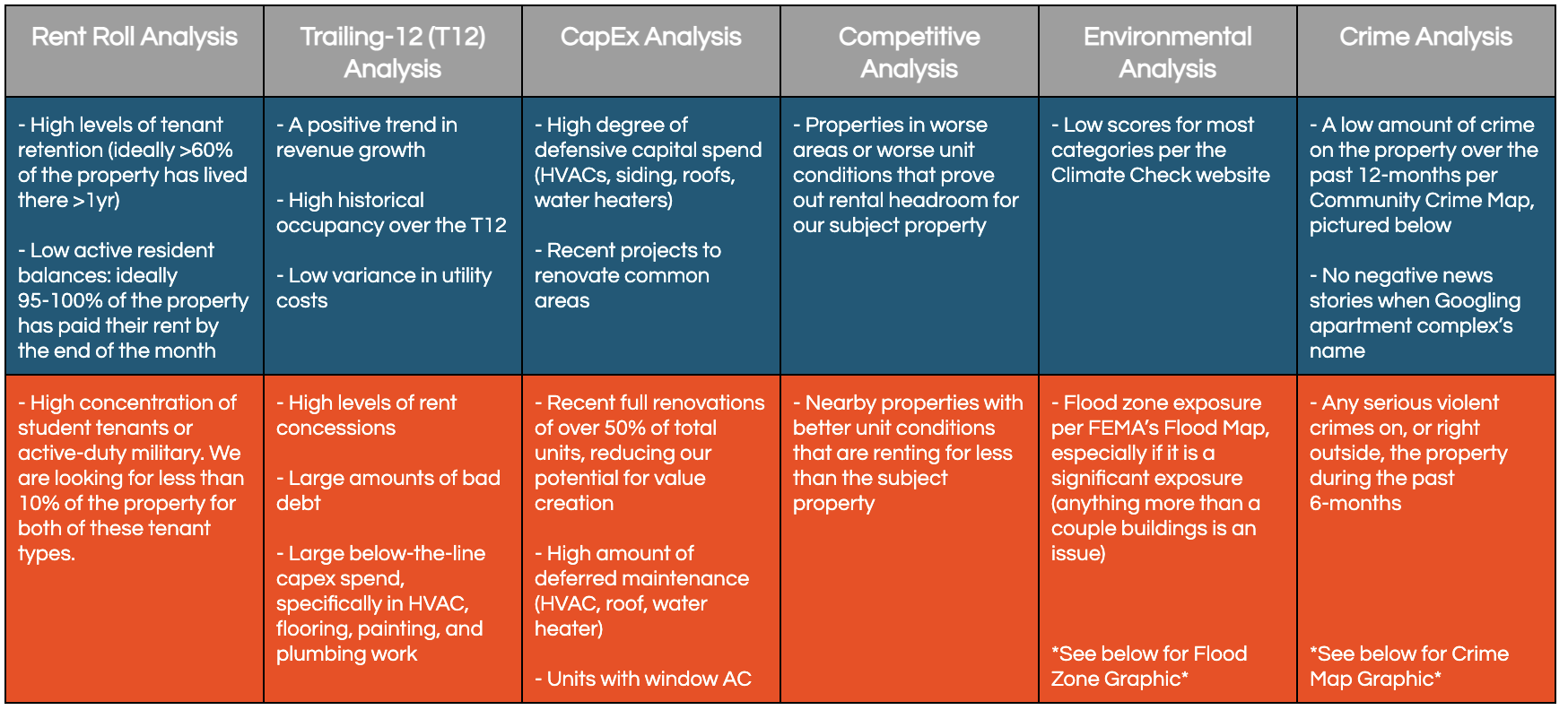

Until this point, our review has been primarily qualitative. This is when the bulk of our quantitative analysis begins. The below table shows various aspects of past property performance and asset characteristics that we analyze. Among many other aspects of the property, the rows that are shaded blue show positive aspects of an asset that we are looking for, whereas the rows that are shaded red show negative aspects and potential deal-killers.

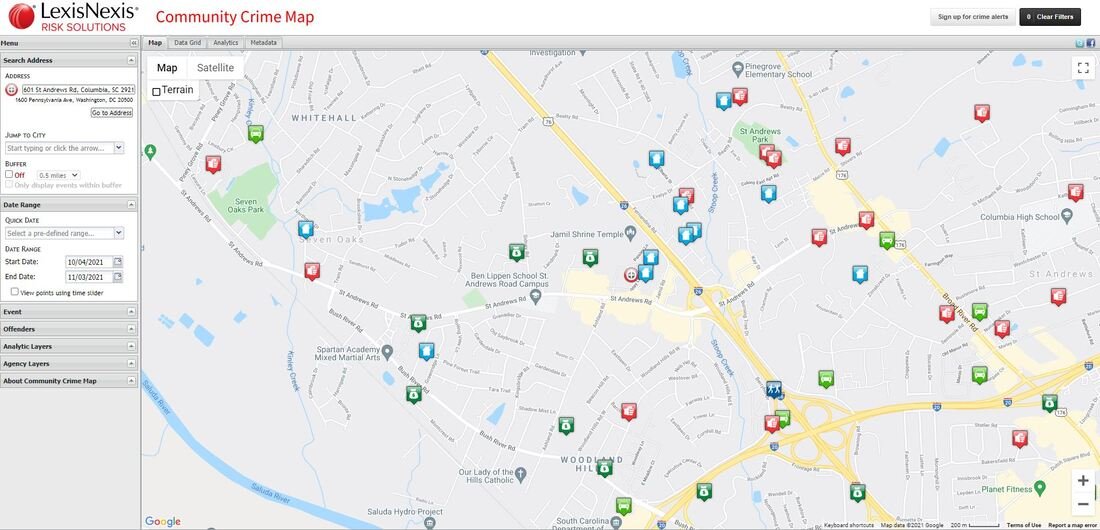

Community Crime Map

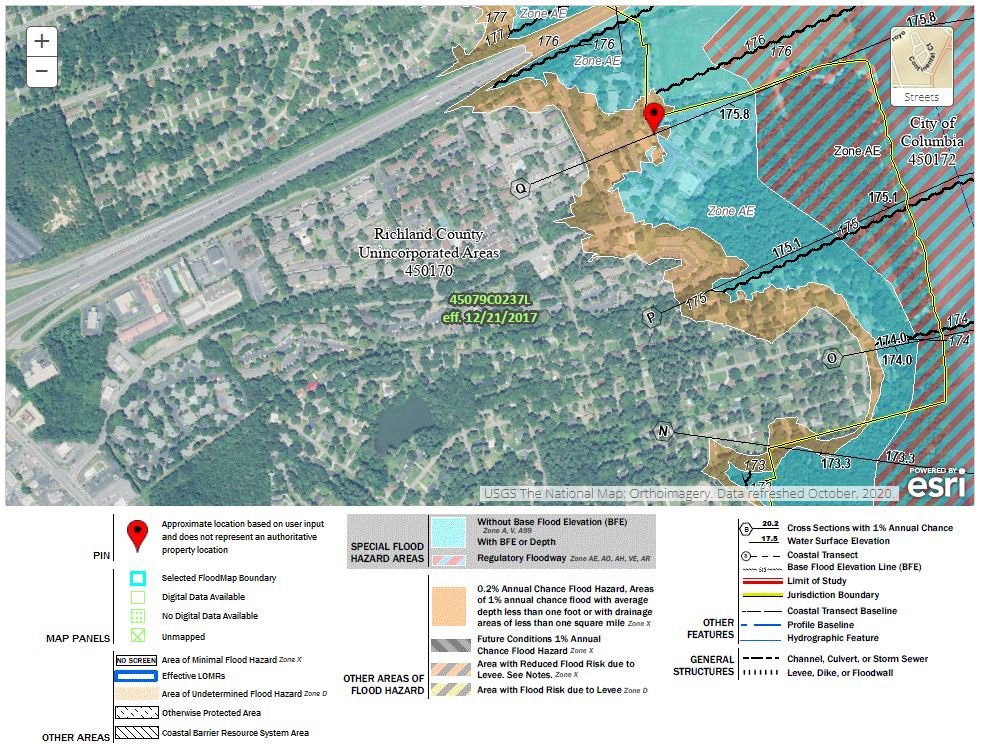

FEMA Flood Map

Site Visit:

Up until this point, we typically have not visited the property, and have based many of our assumptions solely on broker representations, the offering memorandum, financial information, and photos of the property. The purpose of this stage is to not only get a feel for both the physical condition of the community and the quality of the surrounding neighborhood, but also to attempt to verify any of those assumptions that we have made leading up to this point.

Typically, as we work through the aforementioned steps, we accumulate a laundry list of questions – some of these questions are as broad/general as asking the manager to confirm the scope of the previous owner’s capital spend, while other questions are as granular as understanding an outlier month of a specific expense line item. Either way, this stage of our deal analysis allows us to get an answer directly from the property management teams onsite.

Fine-Tuning Deal Underwriting:

By now, both our quantitative and qualitative analysis should be done. At this stage we tighten any overly conservative underwriting assumptions and adjust our underwriting based on our findings from the property visit. Some of these overly conservative assumptions include:

Tightening underwritten occupancy depending on historical performance and our renovation plan

Adjusting our underwritten bad debt level based on historical delinquency trends and current active resident balances

Increasing our market rent assumptions based on unit condition and the condition of the competitive submarket properties.

After we are comfortable with the model that we intend to base our offer price off, we present the deal to our lending team to get their input on likely financing terms.

Bidding Process:

At this stage we submit an offer based on a combination of factors, primarily the following:

What we view as the market cap rate for the asset

How much we can bid to meet our performance expectations for the fund as a whole

Where we expect competitors’ offers to come in based on broker’s guidance.

Based on the above, we establish a “walk-away” price and submit an offer below it. How much is based on the competitive landscape and how well a given asset might fit our portfolio.

PSA, Physical & Operational Due Diligence:

The purpose of our due diligence is to verify every aspect of our underwriting. Some key measures that we take on during this stage are:

Walking 20-30% of units to verify that the units are generally in good condition, and the number of renovated units matches our expectations

Interview and work with on-site staff to understand details of current operations and determine if we want to extend job offers

Comparing actual lease terms for a representative sample of units versus what’s reported on the rent roll, again ensuring there are no discrepancies

Fine-tuning our Repairs & Maintenance and Capital Improvements budgets based on feedback from the managers and findings regarding unit conditions

Close and Take Under Management:

Post-closing, our in-house management team transition into the property management of the project. We send a member or two from the acquisition team on-site for the closing day to make sure the business plan is relayed and assist with every aspect of on-boarding.

Using the strict process outlined above, Ballast Rock has successfully acquired over $100 million of multifamily real estate over the past three years with $55 million year-to-date in 2021.* As we continue to grow and evolve as a company, our origination and acquisition teams finds new ways to improve every step of our process. We believe that as the Southeastern real estate market continues to offer attractive risk-adjusted returns, and our team is in in the flow of opportunities to analyze and acquire to build diversified passive income for our investors.

*Past performance is no guarantee of future results.