Community Solar Lending: Navigating the ITC Sunset and the Opportunities Beyond

The U.S. community solar market recently crossed a milestone that would have seemed improbable a decade ago: more than 10 GW of cumulative installed capacity,[1] delivering savings to hundreds of thousands of households and businesses across 44 states and localities with community solar legislation in place.[2]

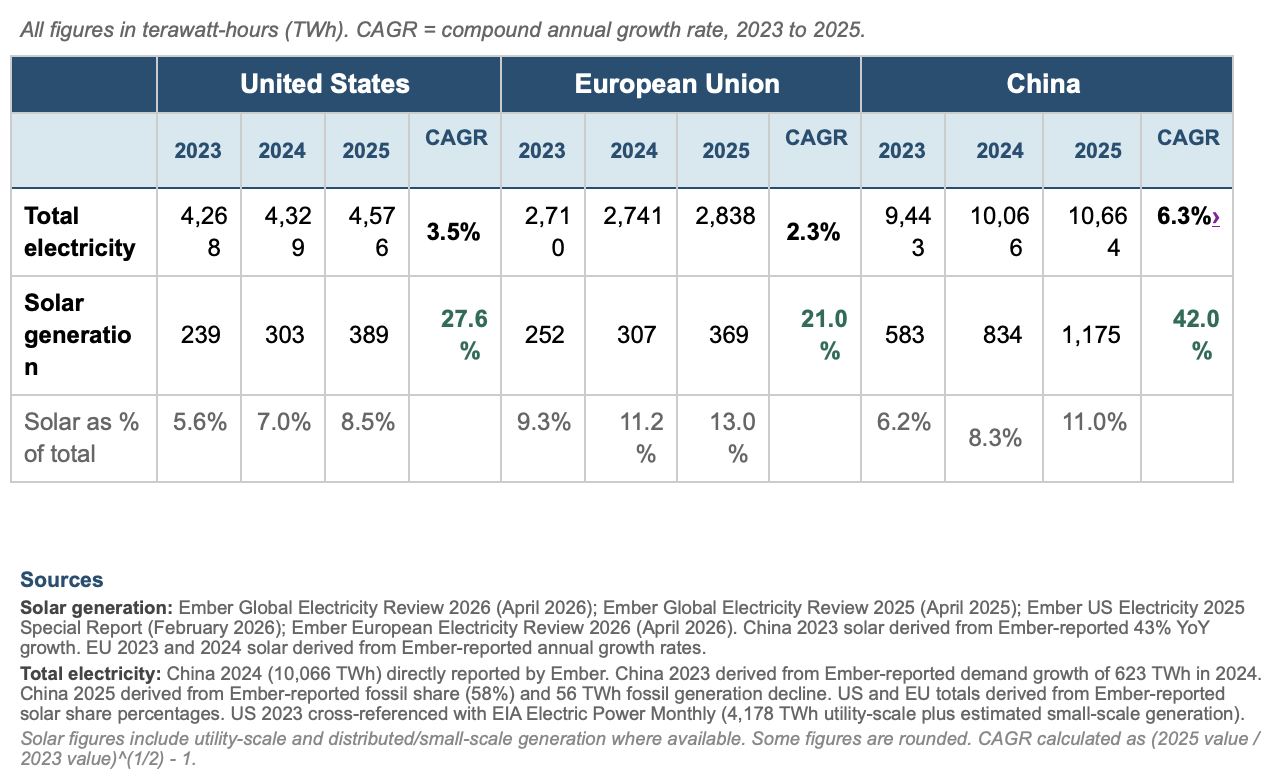

This isn’t an American story alone. As the table below shows, there is a global race to both add generation capacity to the grid and to make solar a significant part of that capacity. China has taken an early lead, adding more solar power than both the US and Europe combined for the last three years. Therefore, the US must continue to expand solar energy as part of its overall strategy for energy security and independence.

Solar Generation vs. Total Electricity Generation (2023-2025)

But milestones can be deceiving, and behind these headline figures sits an American market in the midst of a profound transition, one that is reshaping the competitive landscape for developers, lenders, and investors alike.

For Ballast Rock’s private credit strategy, which provides pre-construction financing to community solar developers, we view this as a multi-decade structural shift in energy infrastructure, not just a short-term trend.

A Market in Flux

Despite the overall growth in national solar generation last year, community solar installations fell 25% in 2025, driven largely by slowdowns in mature markets like New York and Maine.[3] Yet the development pipeline remains substantial, estimated at over 8 GW, with nearly 29% of that capacity already under construction.[4] Analysts project a 12% rebound in installations for 2026, with Illinois and the Mid-Atlantic states emerging as the primary growth engines.[5]

This is directly relevant to our fund, where the loans made to date as well as our active pipeline is concentrated in the states where growth is accelerating. We are lending in the markets that the broader industry is now converging on.

But the more significant story is not cyclical. It is structural.

The OBBBA Clock Is Ticking

The One Big Beautiful Bill Act, signed into law on July 4, 2025, preserved much of the Inflation Reduction Act’s clean energy framework while imposing hard deadlines that have fundamentally changed the pace of development. Projects that begin construction by July 4, 2026, can qualify for investment tax credits under the existing rules, with a four-year window to reach commercial operation.[6] Projects that miss that deadline must be placed in service by December 31, 2027, or forfeit the ITC entirely. There is no phase-out and no partial credit.[7]

For community solar developers, this has created a compressed timeline that is driving an acceleration in demand for exactly the kind of financing our fund provides. The developers we work with are not building large utility-scale projects which can take many years to develop and complete. They are developing portfolios of 1 to 5 MW distributed generation systems that can move from permitting to construction commencement in a matter of months, provided they can access capital quickly. Pre-construction and pre-NTP financing has become the critical bottleneck for many of these developers, and the July 2026 deadline has intensified that pressure.

At the same time, the OBBBA preserved the transferability of tax credits under Section 6418, which is the primary monetization mechanism for the smaller developers we focus on. The ability to sell ITCs to third-party buyers, rather than relying on traditional tax equity partnerships, keeps the community solar capital stack workable for the borrowers we serve. Had transferability been eliminated, as earlier drafts of the legislation proposed, the economics of our target market may have been significantly altered.

Why the End of the Solar ITC Is Not the End of the Opportunity

It is tempting to view the ITC sunset as a purely negative development for solar. In our view, the reality is more nuanced, and in several respects, the post-ITC environment may actually strengthen the case for community solar lending.

Rising energy prices are making solar economics more durable. The cost of electricity in the United States is being driven upward by forces that are unlikely to reverse anytime soon. Data center buildouts, fueled by the AI boom, are placing extraordinary new demands on the grid. The EIA projects the strongest four-year growth in U.S. electricity demand since 2000.[8] Meanwhile, the cost of building new natural gas power plants has surged 66% since 2023, according to a recent BloombergNEF report, driven by materials, labor, and supply chain constraints.[9] For community solar specifically, higher retail electricity rates widen the discount that subscribers receive through solar credits, strengthening the subscriber economics that underpin project revenue. The projects we finance become more valuable, not less, as conventional electricity costs rise.

Battery storage extends the value of solar assets. Under the OBBBA, standalone battery storage remains eligible for the full ITC (Baseline of 30% but as high as 60% project dependent) through 2033, with phase-downs not beginning until 2034.[10] This is a dramatically more favorable timeline than solar alone. For community solar developers, pairing projects with battery storage not only improves project economics and grid value, it also opens a continuing path to federal incentives well beyond the 2027 solar deadline. We expect solar-plus-storage to become the default development model over the next several years, and lenders who understand that evolution will be better positioned to underwrite the next generation of projects.

Reduced competition for well-positioned lenders. The ITC sunset will inevitably cause some developers, particularly smaller or less capitalized firms, to exit the market. It will also cause some lenders and investors who entered the space primarily because of the tax credit arbitrage to pull back. For those of us who are lending against the fundamental economics of community solar projects, and not just the tax credit layer, a less crowded market means better deal flow, stronger terms, and borrowers who are more operationally proven. Market consolidation can be a very good thing for disciplined capital providers.

State-level programs continue to expand. Community solar is ultimately a state-driven market. Twenty-four states and localities have enacted enabling legislation, and new markets in Ohio, Iowa, Pennsylvania, and Michigan are in various stages of program development. If these markets come online, they could add more than 1.5 GW of capacity through 2030, according to Wood Mackenzie,[11] providing a structural growth tailwind even as federal incentives diminish.

Qualified Opportunity Zones: A Potential New Layer

Looking further ahead, the Qualified Opportunity Zone 2.0 provisions introduced by the OBBBA may open a new dimension for community solar investment. The updated program, expected to take effect once Treasury designates new QOZ tracts in 2027, offers significant capital gains deferral and potential exclusion benefits for investments in qualifying projects within designated zones. Community solar installations, particularly in the rural and underserved areas where many zones are located, could be well-suited to these structures. We are actively studying the intersection of QOZ 2.0 with community solar project economics and believe it has the potential to become a meaningful component of the capital stack for future development.

The Risks Are Real

None of this is without risk, and we believe acknowledging those risks is just as important as discussing the opportunity.

Project sale execution risk is a significant risk to monitor. If the market for project acquisitions tightens, if buyer appetite narrows, or if purchase agreement negotiations encounter delays, that directly affects the timing and certainty of payment for sellers of community solar projects. Structuring loans with conservative LTVs and minimum return thresholds provides downside protection, but it does not eliminate the dependency on a functioning transaction market.

State-level policy and regulatory risk are other meaningful factors. Community solar economics are built on state-specific program rules: credit rates, program caps, subscriber eligibility requirements, and utility cooperation. A single policy change, such as a reduction in net metering credits or a program cap being reached, can materially alter project economics in that jurisdiction. A project that works well in Illinois may face entirely different economics in Maryland or New Jersey, and the regulatory landscape can shift with limited advance notice. That’s why it is so important to track proposed and upcoming regulatory changes in the space.

Investment Tax Credit (ITC) compliance and Foreign Entity of Concern (FEOC) risk is a newer but increasingly important consideration. The OBBBA introduced complex FEOC sourcing requirements that developers must satisfy in order to qualify for tax credits. For projects beginning construction in 2026, a minimum of 40% of costs must come from non-FEOC sources for solar and 55% for battery storage, with those thresholds increasing annually.[13] If a project falls out of compliance, the ITC can be disallowed entirely, which would impair project value and potentially the developer’s ability to repay.

Finally, the broader federal policy environment remains uncertain. The 2026 midterm elections and the 2028 presidential race will both have implications for clean energy policy. If Republicans maintain control of Congress, further reconciliation legislation could roll back remaining incentives more aggressively. If Democrats gain ground, some accelerated expiration dates could be reversed. Either outcome reshapes the market. Lenders and investors in this space need to underwrite on fundamentals, not on assumptions about future policy generosity.

Conclusion

Ballast Rock’s Real Estate Private Credit Fund I (“REPC1”) was designed for exactly this market environment. We lend at the pre-construction stage, where capital is scarce and our sector-specific expertise allows us to evaluate projects on their individual merits. We target low loan-to-value ratios and structure downside protection through cross collateralized project portfolios, minimum return thresholds and milestone-based repayment schedules. Our borrowers are experienced developers operating in established state-level community solar programs, and the projects securing our loans are backed by real assets with identifiable paths to completion and sale.

The fund has originated loans across multiple community solar projects in Illinois, with all loans performing as expected. We have additional loans in our near-term pipeline that, if closed, will bring the fund to full deployment. The thesis that small- to mid-size community solar developers are underserved by traditional capital providers has been validated by multiple conversations we have had in the market over the past year, from the Infocast Solar + Wind Finance Summit to direct engagement with developers, co-lenders, and institutional buyers.

Community solar may be niche, but it is not inconsequential. It is a growing segment of American energy infrastructure, supported by durable economic fundamentals, expanding state-level policy frameworks, and increasing demand for distributed generation in an era of rising electricity consumption. The ITC sunset creates urgency in the near term and a more disciplined market in the medium term. For lenders who understand the asset class, the opportunity window remains wide open.

* Ballast Rock Asset Management (“BRAM”), Ballast Rock Private Wealth (“BRPW”), and Ballast Rock Capital (“BRC”) are operating entities of Ballast Rock Holdings (“BRH"), an integrated investment management company. Ballast Rock Asset Management is a non-registered entity. Ballast Rock Real Estate is a wholly owned subsidiary of BRAM. BRPW is a registered investment advisor. BRC is a registered Broker dealer and a MEMBER of FINRA / SIPC. BRC’s registered head office is 460 King Street, Suite 200, Charleston, SC, 29403. Tel: 800-204-2513. To check background information about BRC and its representatives, visit FINRA’s BrokerCheck. Please see important disclosure information in our Form CRS

[1]Wood Mackenzie and Coalition for Community Solar Access (CCSA), U.S. Community Solar Passes 10 GW Milestone Despite Market Contraction, as reported by PV Magazine USA, April 15, 2026. https://pv-magazine-usa.com/2026/04/15/u-s-community-solar-passes-10-gw-milestone-despite-market-contraction/[2]U.S. Department of Energy, Community Solar Market Trends, April 2026. https://www.energy.gov/communitysolar/community-solar-market-trends[3]SEIA and Wood Mackenzie, Solar Market Insight Report: 2025 Year in Review, March 2026. https://seia.org/research-resources/solar-market-insight-report-2025-year-in-review/[4]Wood Mackenzie and CCSA, as reported by SolarQuarter, April 17, 2026. https://solarquarter.com/2026/04/17/us-community-solar-surpasses-10-gw-in-2025-despite-tight-market-conditions-says-wood-mackenzie/[5]Wood Mackenzie and CCSA, as reported by pv magazine USA, April 15, 2026. See footnote 1. [6]PowerFlex, Navigating the OBBBA and Preserving ITC Value for Solar & Storage Portfolios, March 2026. https://www.powerflex.com/blog/navigating-the-obbba-and-preserving-itc-value-for-solar-storage-portfolios[7]Novogradac, OBBBA and the Clean Energy Race Against the Clock, 2026. https://www.novoco.com/periodicals/articles/obbba-and-the-clean-energy-race-against-the-clock[8]U.S. Energy Information Administration, EIA Forecasts Strongest Four-Year Growth in U.S. Electricity Demand Since 2000, January 13, 2026. https://www.eia.gov/pressroom/releases/press582.php[9]BloombergNEF, as reported by TechCrunch, April 27, 2026. https://techcrunch.com/2026/04/27/data-center-demand-drives-66-surge-in-natural-gas-power-plant-costs/[10]Novogradac. See footnote 7. Under the OBBBA, battery storage and other non-solar/wind technologies qualifying for the tech-neutral ITC under Section 48E retain full credit amounts for projects beginning construction through 2033, with phase-downs to 75% in 2034, 50% in 2035, and full sunset in 2036. [11]Wood Mackenzie and CCSA, as reported by Electrek, April 16, 2026. https://electrek.co/2026/04/16/us-community-solar-10-gw-growth-complicated/[12]Wood Mackenzie and CCSA, as reported by pv magazine USA and Electrek. See footnotes 1 and 11. [13]Solar Permit Solutions, Solar Battery Tax Credit 2026: What Changed After the OBBBA, April 2026. https://www.solarpermitsolutions.com/blog/solar-battery-tax-credit-2026